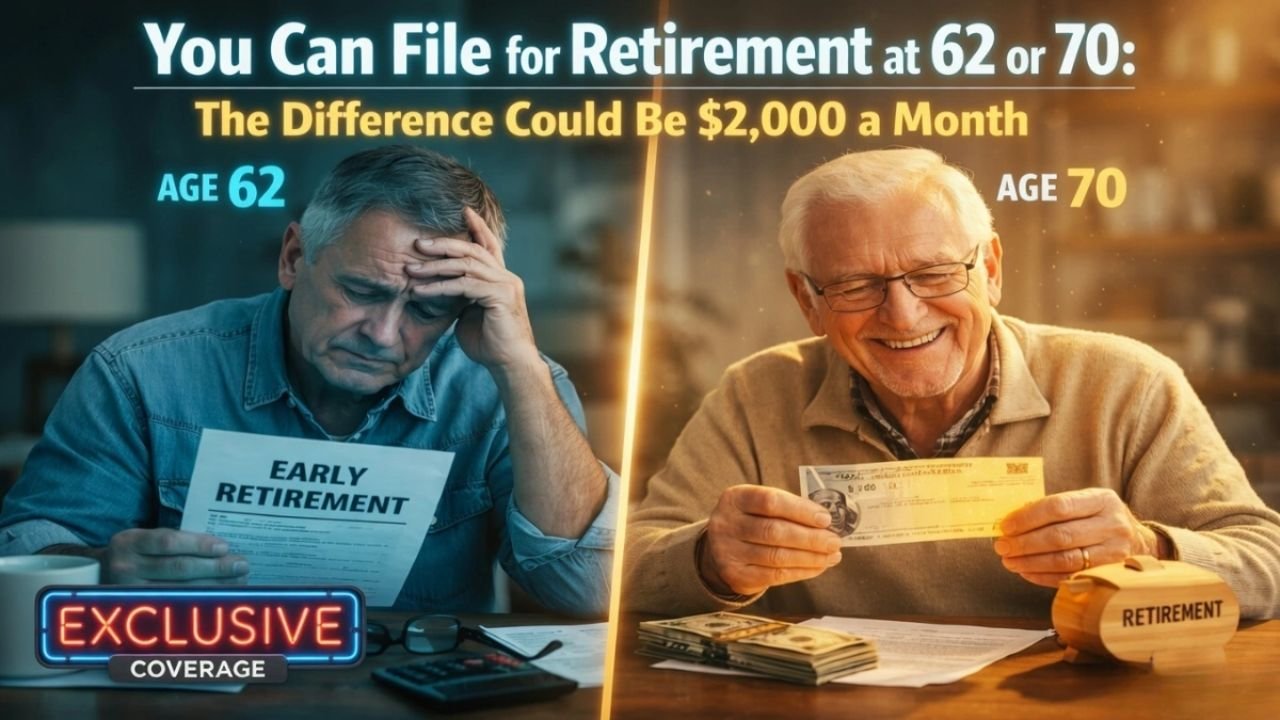

Millions of Americans depend on Social Security Administration retirement benefits as a key part of their financial security. But one small decision—when you start claiming your benefits—can make a massive difference in how much money you receive each month.

Many retirees choose to start benefits at age 62, the earliest possible age. While this provides income sooner, it permanently reduces monthly payments. In contrast, waiting until age 70 can significantly increase your benefits, sometimes by up to $2,000 more per month depending on your earnings history.

Understanding how claiming age affects your payments is crucial for building a stable retirement plan.

Why Claiming Social Security at 62 Reduces Your Monthly Payment

Your benefit amount is calculated based on your Full Retirement Age (FRA). For people born in 1960 or later, the FRA is 67.

Claiming benefits before this age triggers a permanent reduction because the system assumes you’ll collect payments for a longer period.

Key Facts About Early Claims

- You can start benefits as early as age 62

- Benefits may be reduced by up to 30%

- The reduction lasts for the rest of your life

Example Scenario

If your full retirement benefit at 67 is $3,000 per month, claiming early could reduce your payment to roughly $2,100.

Over a retirement spanning 20–30 years, this could mean losing hundreds of thousands of dollars in total benefits.

The Financial Benefits of Waiting Until Age 70

If you delay benefits beyond your Full Retirement Age, you earn Delayed Retirement Credits. These credits increase your monthly benefit by about 8% per year until age 70.

Why Delaying Can Pay Off

Waiting longer can help you:

- Receive higher guaranteed monthly income

- Offset inflation and rising healthcare costs

- Reduce the risk of outliving your savings

- Increase survivor benefits for your spouse

For retirees who expect a long lifespan, delaying benefits often results in greater lifetime income.

Monthly Benefit Comparison by Claiming Age

| Claiming Age | Estimated Monthly Benefit | Difference |

|---|---|---|

| 62 | $2,100 | Reduced benefit |

| 67 (Full Retirement Age) | $3,000 | Standard benefit |

| 70 | $3,720 | Maximum benefit |

In this example, the difference between claiming at 62 vs 70 is $1,620 per month. For high earners, the gap can approach $2,000 or more monthly.

Important Factors to Consider Before Claiming Benefits

Choosing the best time to claim benefits depends on your personal situation.

Key Questions to Ask Yourself

- Do you have enough savings to delay benefits?

- How long do you expect to live?

- Are you planning to keep working after 62?

- Do you need immediate income?

- Will your spouse rely on survivor benefits?

Financial planners often recommend delaying benefits if you can afford to wait, since higher monthly payments can provide stronger long-term security.

How Delaying Benefits Can Increase Lifetime Income

Although early claims provide faster access to money, delaying benefits can result in larger lifetime payouts, especially for people who live into their 80s or 90s.

Additional advantages include:

- Higher inflation-adjusted payments

- Stronger financial protection in later years

- Greater survivor benefits for spouses

Because Social Security includes cost-of-living adjustments (COLA), a larger starting benefit means bigger increases over time.

Quick Tips for Social Security Planning

- Review your estimated benefits statement regularly

- Consider using savings or retirement accounts to delay claiming

- Discuss a claiming strategy with a financial advisor

- Plan for healthcare costs and inflation

Smart planning today can significantly improve your financial security later.

Frequently Asked Questions (FAQs)

1. What is the earliest age to claim Social Security?

You can start receiving retirement benefits at age 62, but your monthly payment will be permanently reduced.

2. What is the Full Retirement Age in the U.S.?

For individuals born 1960 or later, the Full Retirement Age is 67.

3. How much does delaying benefits increase payments?

Benefits increase by about 8% per year for each year you delay after Full Retirement Age until age 70.

4. Is waiting until 70 always the best option?

Not always. It depends on factors like health, financial needs, savings, and life expectancy.

5. Can working after claiming benefits affect payments?

Yes. If you claim before Full Retirement Age and continue working, earnings limits may temporarily reduce benefits.

Final Thoughts

Deciding when to claim Social Security is one of the most important financial decisions in retirement planning. Starting benefits early at age 62 might provide immediate income, but it could permanently reduce your monthly payments.

For many retirees, delaying benefits until age 70 can mean thousands of extra dollars each year and stronger financial protection in later life.

Before making your decision, carefully evaluate your health, savings, and long-term financial goals—because the right choice today can shape your retirement for decades.